Trends in the Semiconductor Industry

1980s

Rise of the Japanese semiconductor industry and strong irritation against it on the U.S.side.Further expansion of consumer electronics markets in Japan, and the first “digital wave.”The focus of the strategies of Japanese semiconductor manufacturers on quality, stable supplies, and achieving competitive prices through active investment, helped significantly raise the status of Japanese semiconductor products. Many U.S. electronics companies started to adopt Japanese semiconductor products, and DRAMs in particular. Meanwhile, the sense of crisis in the US against the success of Japan led to a string of conflicts between the U.S. and Japanese semiconductor industries.

In the field of consumer electronics, VCRs, CDs, and video game machines gained broad popularity. During this period, Japanese consumer product manufacturers had the lead in product supplies worldwide and supported a firm demand for domestic semiconductor products.

“The First Digital Wave” started by the commercialization of Apple and IBM PCs, the second generation of mobile telephony in Europe, and so on, and it then migrated into “the second wave” in the 1990’s.

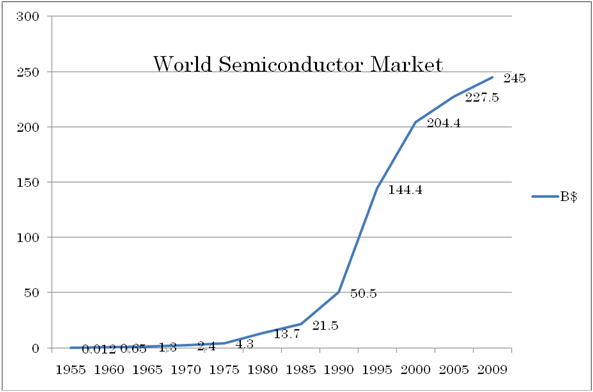

Early 1980's: The global semiconductor market is approximately 3.5 trillion yen, and Japanese manufacturers are still not at the top group of the market.

The 1970s were an era of growth for the Japanese semiconductor industry. Having CMOS LSIs for electronic calculators and watches, analog ICs for consumer electronics, and the silicon transistors as the basis of the business, the development of 64-Kbit and 256-Kbit DRAMs and single-chip microcontrollers made big progress. While the global semiconductor market was large, the share of Japanese manufacturers was only about 25% in 1980, with the U.S. holding more than half of the market.

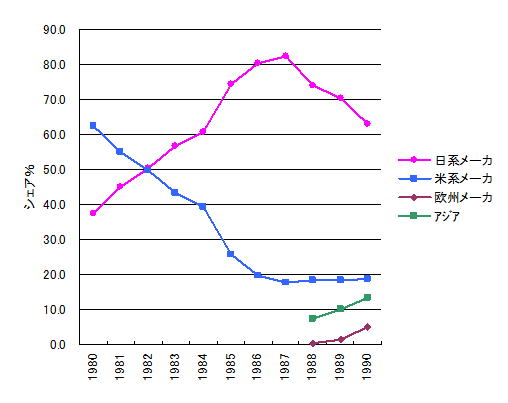

First half of 1980s: DRAMs expand the global share of Japanese manufacturers, who reach the top position for 64-Kbit DRAMs in 1981

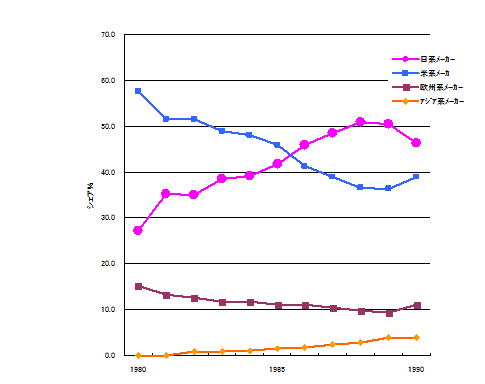

As the U.S. computer industry used more DRAMs, resulting to rapidly increasing demand for DRAMs, many U.S. computer manufacturers adopted made-in-Japan DRAMs, which had been acclaimed for their quality. Japanese DRAMs reached the leading edge in terms of design and process technologies, now gaining high evaluations for quality, delivery, and price. The Japanese share of market in 64K-DRAMs overtook US in 1981, and overall DRAM share reached to 80% in 1987 mainly with 256K DRAMs.

Global Share of DRAM Sales - Japan/US/Asia/EU

1983: Sense of crisis arises in the U.S. semiconductor industry in response to the rapidly increasing share of Japanese manufacturers

The U.S. concerns against Japanese semiconductor industry grew since the late 1970s. SIA was founded, magazines such as Fortune and Business Week published issues appealing the threats of Japanese semiconductor industry, and U.S. semiconductor manufacturers withdrew from the DRAM business. Strong sense of crisis spreaded hand-in-hand with U.S. protectionism.

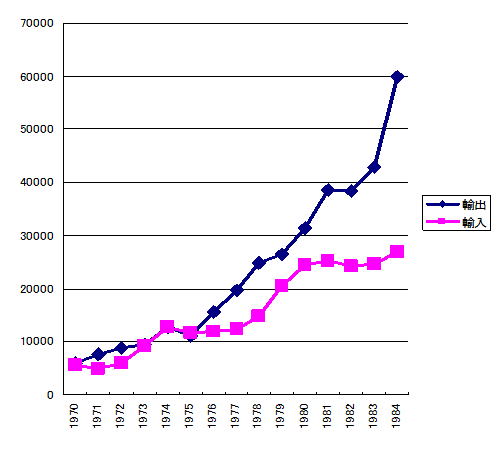

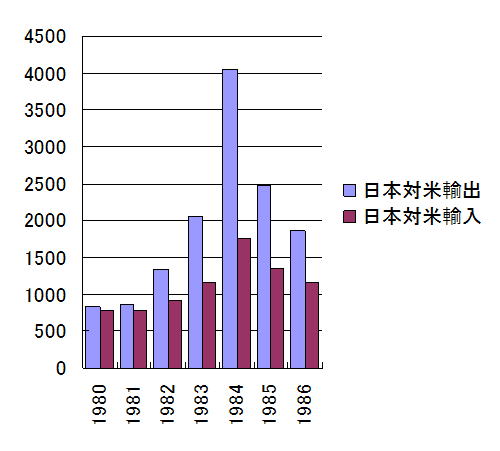

Statistics of Japan’s Trade with U.S.A.

Semiconductor Trade with U.S.A.

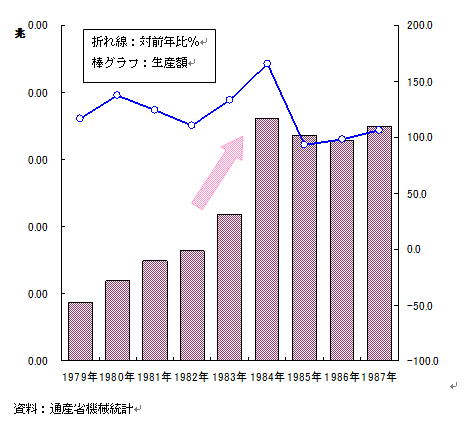

1984: Demand for semiconductor products in Japan reaches 150% of that for the previous year; Japanese semiconductor manufacturers further increase their share with the demand in consumer electronics like VCRs and video-games, and DRAMs for 16-bit PCs

New types of consumer electronics, such as audio-visual equipment, became broadly popular in the 1980s. Production by Japanese manufacturers who were highly competitive in this field rapidly expanded to support the demand for Japanese semiconductor products. Meanwhile, the growing demand for DRAMs triggered by the boom in 16-bit PCs allowed Japanese semiconductor manufacturers to increase their share of the global market.

Japan’s Production Volume of Semiconductor

Transitions of Japanese and U.S. DRAM Shipment Shares

1985: The SIA and U.S. manufacturers file a series of dumping lawsuits against Japanese semiconductor manufacturers

In June 1985, the SIA filed a dumping lawsuit against Japanese semiconductor manufacturers with the United States Trade Representative (USTR) under section 301 of the U.S. Trade Act of 1974.

This was followed by further dumping lawsuits, by Micron against Japanese 64-Kbit DRAMs and by Intel against Japanese EPROMs. In 1986, the International Trade Commission (ITC) ruled that Japanese 64-Kbit DRAMs had damaged the U.S. semiconductor industry.

August, 1985: Japanese and U.S. governments start talks on the semiconductor problem;

September 1986: Signing of the U.S.–Japan Semiconductor Trade Agreement

This agreement defined the following three conditions: (1) promotion of greater access to the Japanese market by foreign semiconductor companies, (2) prevention of dumping, and (3)suspention of anti-dumping inquests by US government. To expedite the market access, the International Semiconductor Cooperation Center (INSEC) and User’s Committee of Foreign Semiconductors (UCOM) were established in 1987 and 1988, respectively.

1985: Establishment of EUREKA in Europe, with IMEC having been established in 1984.

To minimize the technology gap between Europe on the one hand and the U.S. and Japan on the other, the then-EC invested $5.8 billion in 1984 for the creation of EUREKA, a collaborative program to support research and development into semiconductor technologies. Also in 1984, the Belgium government founded IMEC to strengthen the field of microelectronics by encouraging collaboration between industry, government, and universities, including international partnerships.

1985: The Rise of Wintel

Wintel is a compound word of Windows and Intel, which is a common name for computers with Microsoft's Windows series operating system and Intel microprocessors, or the relationship between Microsoft and Intel. PCs with Microsoft's operating system and Intel CPUs have begun to dominate a significant larger market share from around 1985.

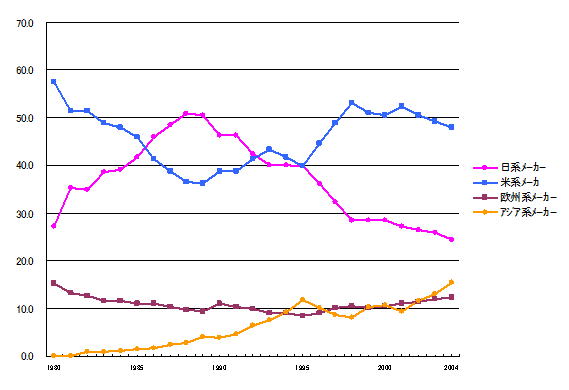

1986: Japan becomes the biggest supplier in the global semiconductor market, surpassing the U.S.

Japanese manufacturers expanded their share due to increased memory production (such as DRAMs) and stable domestic demand for consumer electronics. The top three manufacturers in 1986 were NEC, Toshiba, and Hitachi, and six out of the top ten were Japanese manufacturers.

Regional Supply Share of Semiconductors

1987: The U.S. government imposes tariffs under section 301 of the 1974 U.S. Trade Act, retaliating for non-observance of the U.S.–Japan Semiconductor Trade Agreement.

This incident was the second round of the conflict between the U.S. and Japanese semiconductor industries. In March 1987, the U.S. government made an announcement that it would impose tariffs on Japanese products in retaliation for Japan's failure to allow more foreign semiconductor products into the market and for ongoing dumping of Japanese semiconductor products in other countries. The Japanese government responded by encouraging more imports of American semiconductor products and raising the prices of Japanese products in other countries. With an upturn in the global market and an apparent improvement in the price situation in other countries, the U.S. government eliminated some sanctions in November 1987.

1987: Foundation of Semiconductor Manufacturing Technology (SEMATECH) in the U.S.

In the late 1980s, the U.S. utilized several industry associations and cross-industrial organizations such as the SIA, SEMATECH, and Semiconductor Research Corporation (SRC) to take a series of strategic actions to counter Japan after the Japanese share surpassed that of the U.S. semiconductor industry. This move led to a recovery of the U.S. semiconductor industry, which once again surpassed the Japanese semiconductor industry in 1993.

World Supply of Semiconductor by Region (~ 2004)