Trends in the Semiconductor Industry

2000s

1. Rise of BRICs market and intensified globalization

2. Standerdization, commoditization and lower prices for semiconductor products

3. A third digital revolution leading to integrated equipment of PC, Internet, digital consumer electronic, and wireless erminals, etc.

4. The business environment for vertically integrated Japanese device manufacturers worsened as the semiconductor industry came to be based on a flatter and horizontally divided structure.

2000: The global semiconductor market significantly rises to 22.5 trillion yen

The top three manufacturers were Intel, Toshiba, and TI, with Samsung in the fourth place. However, TI and Toshiba both suffered from the recession in 2002 and dropped from the top three. Samsung then surged to second. Samsung secured the same position throughout the 2000s, except in 2007.

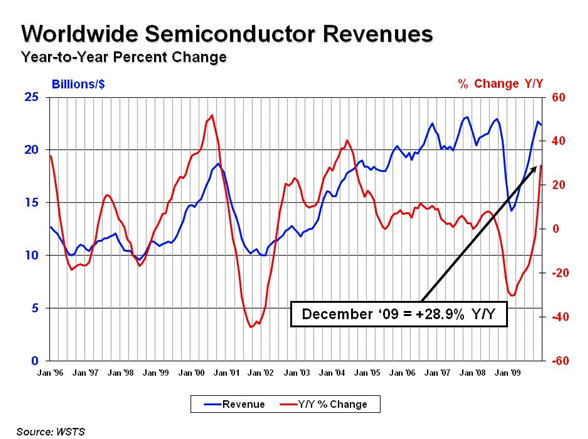

Worldwide Semiconductor Revenue - Year on Year Percentage Change

Early 2000: Start of government-industry projects in Japan with main focus to fabrication technologies

120 billion yen in total was invested on the following projects: ASUKA (2000), Mirai (2001), HALCA (2001), ASPLA (2002), EUVA (2002), DINN (2001), and CASMAT (2003).

Early 2000: Fabless semiconductor companies gain further prominence; growth in semiconductor products for telecommunications

Technologies for broad-band communications developed. These included FTTH and xDSL for fiber, and WiFi, WiMax, and 3GGSM for wireless communications. Qualcomm and Broadcomm in the U.S. outsourced chip manufacturing to foundry companies TSMC and UMC. The results of such collaboration between horizontally divided organizations overwhelmed Japanese integrated device manufacturers.

Early 2000s: Competition in the markets for consumer electronics, EDP equipment, and communications equipment becomes increasingly severe; significant changes to the structure of the semiconductor market

The demand for semiconductor products changed due to the rise of BRICs and the tendency to pursue quick turnaround times (QTATs) and low costs: the popularity of general-purpose products and low-price application-specific standard products (ASSPs) increased while that of application-specific integrated circuits (ASICs) declined. Expansion of the Asian market and cost reductions accelerated as Asian electronics manufacturing service (EMS) and original design manufacturing (ODM) companies were entrusted with direct purchasing of semiconductor products.

January 2002: Toshiba withdraws from the DRAM business to focus on NAND flash memory

South Korean manufacturers had been in pursuit of Japanese manufacturers (leaders in the DRAM field in the late 1980s) since the early 1990s. Once Samsung took the lead in 1994, hardships continued for the Japanese manufacturers.

2002: NEC separates its semiconductor division to form a new company, NEC Electronics

2003: Hitachi and Mitsubishi found Renesas Technology as a joint venture centered on SOCs

These events highlighted structural reforms among Japanese manufacturers, including mergers and the separation of divisions.

In April 2010, Renesas Electronics was established through a merger between NEC Electronics and Renesas Technology.

2003: Start of digital terrestrial broadcasting

The market for liquid crystal display (LCD) televisions started to expand. As the demise of the production of CRTs approached, the number of LCD televisions being produced increased to the scale of 200 to 250 million units per year.

2005: Recovery of the global semiconductor market to the scale of 25.1 trillion yen

The top three manufacturers were Intel, Samsung, and TI, followed by Toshiba in fourth place. Microfabrication technology advanced to 90 nm. TI successfully recovered market share through expansion in DSP, analog, RF, and power devices by adopting a fab-lite strategy to focus on upstream design.

2007: Exploding number of mobile phones worldwide reaches 3.5 billion

There were 3.5 billion mobile phones in use worldwide, constituting one for each person in 50% of the entire world’s population (in Japan, 75% were using mobile phones). Other worldwide penetration rates were 35% for PCs (75% in Japan), 35% for the Internet (70% in Japan and 35% in China), and 18% for broadband equipment (60% in Japan).

2008: 21 years after its establishment, TSMC achieves a 50% share of the global foundry market.

In the global semiconductor rankings, TSMC was 10th in 2002 and equal 6th in 2007. The trend towards horizontally divided businesses accelerated the move in the semiconductor industry towards only focusing on a limited range of processes. Looking at sales in 2007, we see that foundry company TSMC (900 billion yen), assembly and testing company ASE (360 billion yen), fabless company Qualcomm (660 billion yen), IP-design company ARM (60 billion yen), and EDA vendor Cadence (190 billion yen) all made stable profits despite the recession.

Late 2000s: Emergence of “more-than-Moore” semiconductor technologies and diversification of product categories

Diverse products such as ASSPs, FPGAs, 3D SIP/SOCs, analog ICs, power devices, MEMS, sensors, LEDs for lighting, memory devices, MPUs, and ASICs emerged and evolved in ways not constrained by Moore’s Law.

Late 2000s: Facilities and R&D require enormous expenditures due to further microfabrication and integration of semiconductors

Only Intel, Samsung, TSMC, and Toshiba’s Yokkaichi operation made large-scale investments. Other manufacturers employed foundry companies such as TSMC, adopted the fabless business model, or sought joint development or alliances to limit investments and diversify risks.

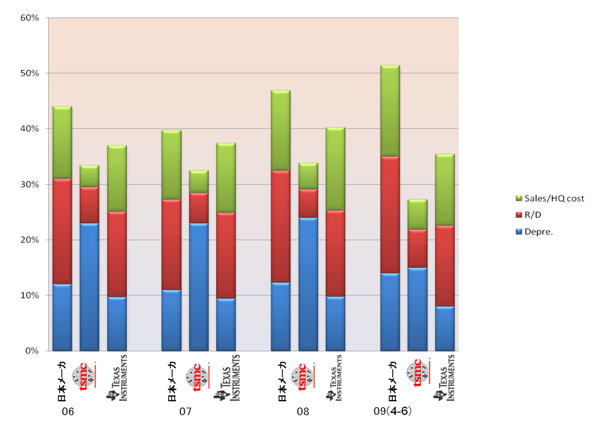

Comparison of Fixed Costs of Japanese and Foreign Companies

2008: Digital video remains a major field for Japanese consumer electronics products; Sony’s Blu-ray Disc becomes the world’s de-facto standard; Japan has an 80% share of the global market for digital cameras

Japanese electronics manufacturers still have the ability to create new products and provide a premium brand image in the field of stand-alone digital consumer electronics. However, once mass production starts, the market share (except in the case of digital cameras) tends to drop as competitors, such as South Korean manufacturers, set out in pursuit. The disconnection between consumer electronics and domestic demand for semiconductor products also presents a difficulty.

200GB Blue Ray Disc from Sony

2009: The global semiconductor market declines by 11% to sales of 21.5 trillion yen; same top three manufacturers as in 2008: Intel, Samsung, and Toshiba

Microfabrication advanced to 45 nm. Fabless companies further expanded their shares: Qualcomm jumped from 8th to 6th, Broadcom from 14th to 13th, and Taiwan’s Mediatek from 24th to 15th.

Qualcomm was particularly successful in becoming the leading fabless company, making a profit of 600 billion yen over the 25 years since its foundation and posessing 11,000 U.S. patents related to CDMA wireless technology.