Trends in the Semiconductor Industry

1990s

Struggling Japanese semiconductor industry and the second wave of digitalizationThe Japanese semiconductor industry struggled with the regulations defined by the U.S.-Japan Semiconductor Trade Agreement such as Fair Market Value (FMV) and allowing more foreign semiconductor products into the market. This situation continued until the agreement expired in 1996.

The Japanese share dropped when South Korean and Taiwanese manufacturers joined the global semiconductor market and U.S. manufacturers regained competitiveness. South Korea reorganized its semiconductor industry and actively encouraged development and investment after the financial crisis of the late 1990s, rapidly raising its status in the field of DRAMs.

Personal computers, peripheral equipment, and office equipment were the major forces boosting demand for semiconductor products. In particular, a cycle of demand for semiconductor products alternating between rising and falling greatly affected the semiconductor demand; rising with purchases of new PCs every time Windows OS was upgraded, and falling as the reaction to the boost. Furthermore, demand in the global semiconductor market shifted to PCs and peripheral equipment produced in the U.S. and Asia rather than for consumer electronics, where Japanese manufacturers held the initiative. For this reason, regional demand for semiconductor products dramatically increased in Asia.

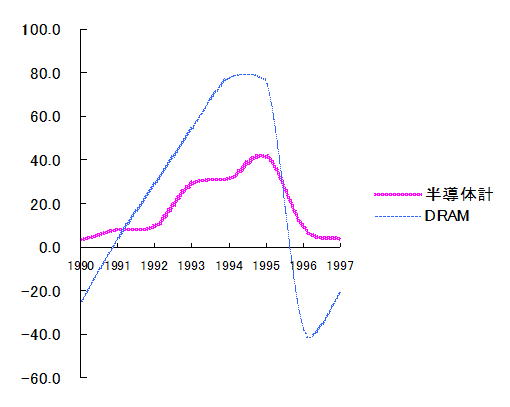

From 1993 to 1996: The global semiconductor market maintains 30% growth per annum in the Windows-PC boom

In 1993, Intel released the Pentium series and Microsoft released Windows 3.1. Significant improvement in video processing further increased the demand for PCs and peripheral equipment such as printers. This led to more demand for MPUs, DRAMs, and semiconductor products for use in peripheral equipments. The release of Windows 95 in 1995 and the general trend towards office automation (initially started by American financial corporations) also accelerated demand.

Year to Year Growth of Global Semiconductor Market

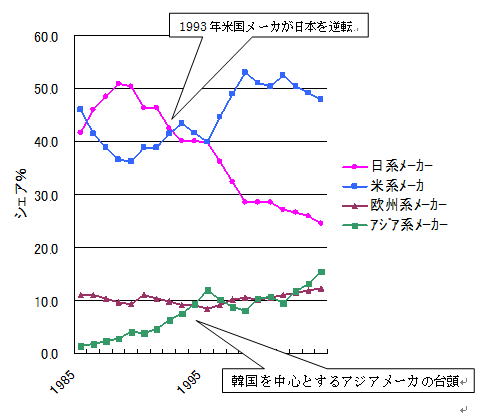

1993: U.S. manufacturers retake leadership in market share from Japanese manufacturers; rise of other Asian manufacturers

The U.S. retook first place with a 43% share of the global semiconductor market. Japan was second with a 40% share. The top manufacturer was Intel, which had marked success, mainly with MPUs. Intel was followed by NEC, Toshiba, Motorola, and Hitachi. Meanwhile, South Korean and Taiwanese manufacturers expanded their ability to supply customers and became global semiconductor companies. In 1994, South Korea and Taiwan together took a 10% share of the global market, equivalent to that of Europe. The share of Japanese manufacturers dropped to 28% by the end of 1990s due to the success of the U.S. and the rise of South Korean and Taiwanese manufacturers.

World Supply of Semiconductor by Region (~ 2004)

1994: Semiconductor Mid-term Vision Committee reports the results of surveys (from 1993 to 1994)

In April 1993, the Semiconductor Mid-term Vision Committee was set up within the Electronic Industries Association of Japan (EIAJ) with one year term. Since most industries in Japan were suffering from economic depression due to the yen appreciation around that time, the risc of hollowing out and uncertain employment of the semiconductor industry became realistic one. Several projects were being undertaken in response by enterprises in the Japanese semiconductor industry. From among these, the Semiconductor Mid-term Vision Committee proposed the establishment of a permanent think-tank for the Japanese semiconductor industry, and this later was realized as the Semiconductor Industry Research Institute Japan (SIRIJ).

1994: Establishment of the Semiconductor Industry Research Institute Japan (SIRIJ)

In response to the suggestion from the Semiconductor Mid-term Vision Committee, the Semiconductor Industry Research Institute Japan (SIRIJ) was founded as a permanent think-tank by ten semiconductor manufacturers as a voluntary organization in April.

The proposals initially made by SIRIJ included establishing joint-research projects to solve problems and led to practical activities such as strengthening the design capabilities (for product development) of the respective manufacturers and the establishment of Semiconductor Leading Edge Technologies, Inc. (Selete) and the Semiconductor Technology Academic Research Center (STARC).

1996 to 1997: Recession for the semiconductor industry (DRAMs)

The market for PCs rapidly entered a correction phase due to a backlash against the accelerated trend to office automation and PCs that was started by Windows 95. In particular, the supplies of DRAMs were excessive, and many semiconductor manufacturers were forced to adjust their production and suffered a severe downturn. This recession in the DRAM sector also led many Japanese manufacturers to withdraw from the DRAM market: Fujitsu in 1999, Hitachi and NEC (which split off their DRAM sections into a new company, Elpida Memory) in 1999, and Toshiba in 2001.

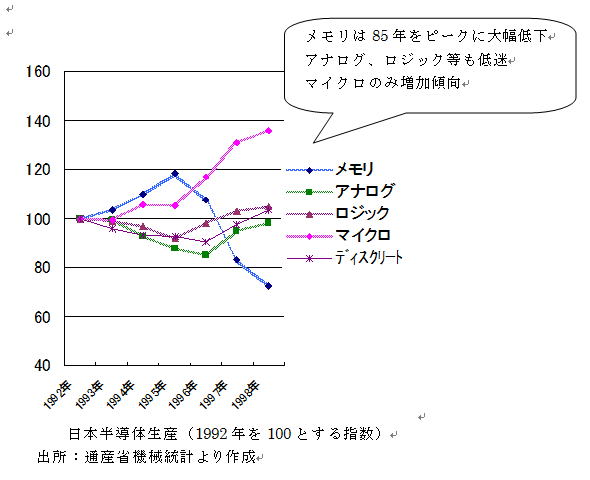

Japanese Semiconductor Production by Product Categories (1992 = 100)

1996: Talks on expiration of the U.S.-Japan Semiconductor Trade Agreement

Vancouver Agreement in July, 1996; Replacing the existing governmental agreement, EIAJ and SIA made an industry-industry agreement, “Agreement on Internatioanal Cooperation Regarding Semiconductor” as the anti-dumping guideline between industries and request of voluntary commitments from corporate members.

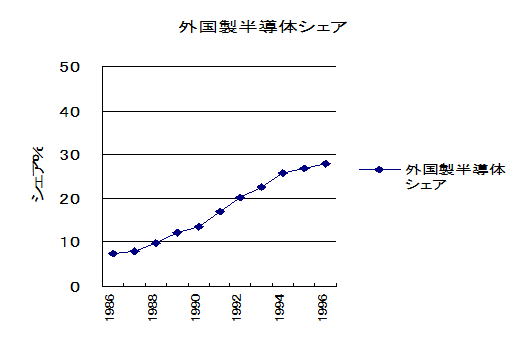

Forein Semiconductor Share in Japan

1997: First meeting of the World Semiconductor Council (WSC)

Based on a suggestion in the joint agreement between the U.S. and Japanese semiconductor industries that was signed in Vancouver, the first meeting of the WSC was held in Hawaii. The initial members were the EIAJ, SIA, the European Electronic Component Manufacturers Association (EECA), and the Korean Semiconductor Industry Association (KSIA), and these were later joined by the Taiwan Semiconductor Industry Association (TSIA) and the China Semiconductor Industry Association (CSIA).

The aims of the WSC are to solve problems in the semiconductor market and to examine how to maintain the healthy growth of the semiconductor industry while adhering to WTO rules. The WSC summarizes its results as proposals to Governments/Authorities Meetings on Semiconductors (GAMS; the membership consists of the relevant governments and authorities) to prompt talks between governments leading to improvements in their systems and policies.

1997: Asian financial crisis

The economies of Thailand, Malaysia, Indonesia, and South Korea were severely affected by the financial crisis, and the demand for semiconductor products decreased.

The effect on the businesses of South Korean manufacturers was critical because they had been expanding their market share through active investment and competitive pricing with a focus on DRAMs. Some manufacturers experienced major structural changes under the guidance of the South Korean government.

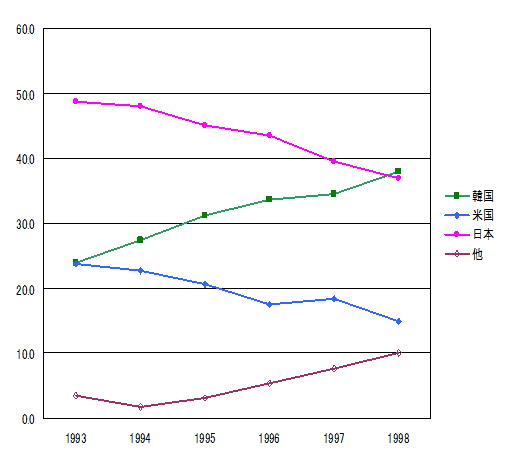

1998: South Korean manufacturers surpass Japan in the global DRAM market

While Japanese and U.S. manufacturers struggled in the DRAM market, South Korean manufacturers became dominant as they intensively promoted development and investment in plants and equipment in the field of DRAMs, surpassing Japan in 1998.

Worldwide Share of DRAM - Koreans Overtook Japan